This post was written by Simon van Norden of HEC-Montréal

Paul Krugman picked a fight with Ken Rogoff today. The subject is how much to worry about the run up in government debt in the US and Europe. The Financial Times has been running a series of articles on the subject and Krugman claims that Rogoff "has been giving seriously bad policy advice." For macro wonks like me, this is better than the World Cup. Both are very clever men, both work hard to link theory and policy, and both can rightfully claim this kind of macroeconomics/international finance/economic history/growth is their forté.

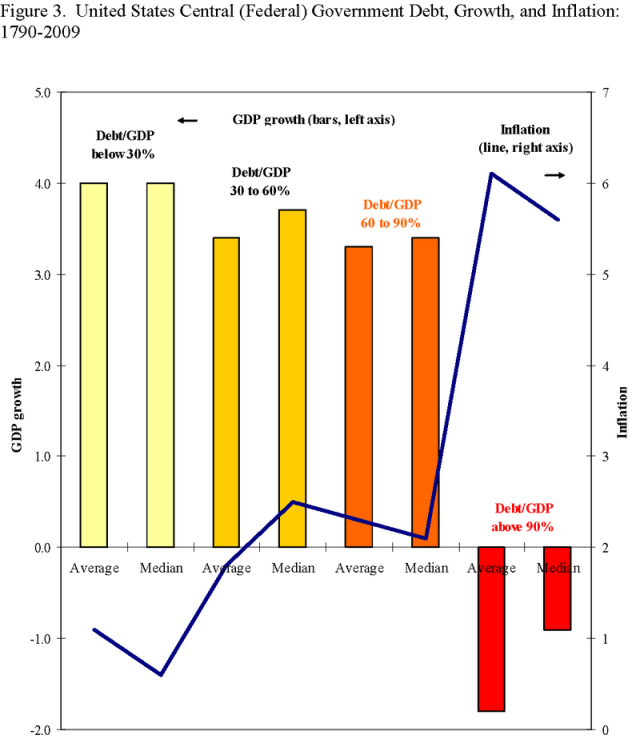

Krugman is pretty specific in his criticism; he's picking on the analysis in one specific very recent paper by Rogoff and Carmen Reinhart that's making the rounds. The paper has a striking graph

With this and other data, Rogoff and Reinhart document that, historically, there is not much of a relationship between government indebtedness and growth except for the over 90% of GDP group. For debt loads up there, growth seems quite a bit lower. (In the case of the US, inflation looks higher as well.)

Krugman doesn't dispute the data; he disputes Rogoff's use of it to urge for fiscal restraint. I'm trying to understand their conflicting points of view, but here's my take on it so far.

1. Krugman is complaining that people are fixating on the 90% mark as if it is a critical threshold. To be sure, he's careful not to accuse Rogoff of arguing that, and there's nothing in the above paper to suggest that it is. This seems to be more about how others are using the results rather than what Rogoff wrote.

2. Krugman claims that the relationship is not robust. He argues that the US data for high debt levels are dominated by one brief period after WWII and that relevant conditions then (e.g. millions of demobilized soldiers, shift from military to civilian production, devastated European and Asian economies) might be different from conditions in the foreseeable future. Reinhart and Rogoff's paper presents evidence for many other countries. They also find lower growth for high-debt (i.e. >90% Debt/GDP) advanced economies after WWII, as well as for high-debt emerging economies over that period. However, they also conclude that "debt thresholds are importantly country-specific and as such the four broad debt groupings presented here merit further sensitivity analysis."

One feature of the Reinhart-Rogoff paper that strikes me is that they only seriously consider the possiblity that debts cause low growth. They mention various plausable mechanisms (e.g. high taxes.) But Debt/GDP is a ratio: if it gets big, that's because the numerator grows faster than the denominator. There's really not much discussion of the possiblity that causality goes the other way; that countries with poor growth get into debt trouble.

That's odd, because another paper in a widely-cited journal documented historical links between US growth and debt management. They looked at how the US Debt/GDP has varied over the centuries and found that, on average, drops in the ratio had very little to do with fiscal tightening and were instead dominated by rapid growth. This was particularly true for the recovery from those very high debt levels after WWII; they note that of the drop in Debt/GDP from 115% in 1945 to 27% in 1975, GDP growth alone would have lowered the ratio to 39%. (Who are these radical liberals? One is the author of the most popular macroeconomics textbook another runs the CBO.)

I'm keen to see how this debate evolves. However, my bottom line right now is a simple point that I made last week in comments to another post. In the absence of further deficits, Debt/GDP will grow if the interest on the debt (r) is bigger than the rate at which the economy grows (g). Right now, the US government can borrow for 20 years at a real interest rate of 1.8%. Since 1929 (i.e. including the Great Depression), the US economy has grown at a real rate of 3.65% and has never averaged growth of less than 2.5% annually over any 20 year period. That's a powerfully stabilizing force; it means just balancing the budget should be enough to get the Debt/GDP ratio dropping by 1.5-2% per year…..if growth continues.

I’m having trouble with your two ‘radical liberals’ links.

Make that all of your links. Except the ‘Simon van Norden’ one at the top.

Oops – should have checked. Simon!

It’s a good article, though. Krugman vs. The World is one of my favourite sports channels too.

Links are fixed!

When you say “GDP growth alone would have lowered the ratio to 39%,” do you mean “GDP growth and inflation”?

Because I’m having trouble squaring the graph with the claim that growth alone would have lowered the debt/GDP ratio from 115% to 39%. If the >90% section of the graph is dominated by post-WWII data, then doesn’t that suggest growth was negative after WWII while debt/GDP was over 90%? And so doesn’t that mean it must have been inflation that lowered debt/GDP from 115% to somewhere below 90%, and then growth took over from there?

As DeLong has now shown, there was only one period where this ratio went over 90%. That was right at the end of WWII which was followed by demobilization, which caused output to go down. So in the case of the United States Rogoff is generalizing on the basis of one single highly unrepresentative case.

See http://www.j-bradford-delong.net/

Krugman, of course, has already made this point several times.

For example, in http://krugman.blogs.nytimes.com/2010/03/12/debt-and-transfiguration/:

“What I think I’m seeing, although I haven’t tested this carefully, is that the causal relationship largely runs from growth to debt rather than the other way around. That is, it’s not so much that bad things happen to growth when debt is high, it’s that bad things happen to debt when growth is low. ”

or in http://krugman.blogs.nytimes.com/2010/05/27/bad-analysis-at-the-deficit-commission/:

“And I suspect that much of the rest of their result reflects reverse causation: Japan had low debt and fast growth before the 90s, high debt and slow growth since, but surely we believe that Japan’s financial crisis is what both slowed growth and increased debt; similarly, the onset of Eurosclerosis is what led both to slowing growth and higher debt in Europe. And here’s the thing: Reinhart and Rogoff have not, as far as I can tell, made any effort to disentangle the causation here.”

When repeating someone else’s arguments it’s poor form not to acknowledge them. Even poorer form to present yourself as adding something new to that person’s argument without putting in the tiny effort required to find out that they’ve already made the same point (the links to the posts I cited can be found by following the link from a post Krugman made just yesterday).

And it’s remakably silly to think a guy like Krugman wouldn’t have thought of such an obvious point.

Ryan: Inflation is interesting, esp. since the graph shows that US inflation during this period averaged about 4%. But remember that Debt/GDP is a ratio: we can measure them both in real terms or both in nominal terms and get the same results. The key is that this is a race between the growth rate of the numerator (r if the primary deficit is zero) and the growth rate of the denominator (g). Inflation tends to make both increase in nominal terms. But there is also a third way to get the deficit down below 90%: run surpluses for a few years.

Roland Buck: Yup, DeLong has usefully brought out his Debt/GDP ratio graph to remind us of what the data look like. (I’m not sure why he feels I’m “Off”, but there you go.)

Adam P: I did not know that I was repeating Krugman’s arguments. Thanks for the links to Krugman’s previous posts. I’m not aware that (i) he makes the point that R&R discuss only causation from debt to GDP growth, and (ii) that he cites the historical analysis of US debt dynamics that I cite above. I’m sure you’ll speak up and let us know if I missed that. Cheers,

Simon: ” I’m not aware that (i) he makes the point that R&R discuss only causation from debt to GDP growth…”

Krugman quoted in my comment just above:”And here’s the thing: Reinhart and Rogoff have not, as far as I can tell, made any effort to disentangle the causation here.”

True Krugman doesn’t cite the specific paper you cite but if that was your whole contribution you should have just said so.

Adam P: There is a difference between not “disentangling” causation on the one hand and discussing only causation from debt to growth on the other hand. Tell me what part of this distinction you don’t understand and I’ll see if I can explain it in terms you can understand.

Now, now.

Hey! I’m just sticking to the facts of the discussion. Not people’s personal habits, morals, etiquette, etc. None of that. Just business.

“just balancing the budget”

Yeah, once out of the box, it’s easy.

Krugman: “What I think I’m seeing, although I haven’t tested this carefully, is that the causal relationship largely runs from growth to debt rather than the other way around. That is, it’s not so much that bad things happen to growth when debt is high, it’s that bad things happen to debt when growth is low. ”

I suspect that the latter is the case. However, to be precise, we might say, “It’s that bad things happen to debt/GDP when growth is low.” When you put it that way, well, big DUH! If debt is relatively slow to change, while GDP is a measure of growth, then of course things happen to the ratio when the numerator changes a little and the denominator changes a lot. And those things are bad if high debt/GDP is considered to be bad.

But why is it considered to be bad? It is considered to be bad because of the presumed causal relationship where a high debt/GDP ratio causes low GDP. If causality runs the other way, then isn’t the deficit/GDP ratio more of an indicator of how low growth affects the debt? Now, we know that, in the developed world, low GDP tends to trigger “automatic stabilizers” that increase the deficit, and that, OC, increases the debt.

But isn’t it true that debt may be a drag on GDP? Through interest payments? At least, through interest payments to foreigners? If so, then why not a ratio of debt-service/GDP or foreign-debt-service/GDP?

Why do people even care about debt/GDP at all?

With regards to causality, has anybody tried to correlate debt/GDP ratios with indicators of business and consumer confidence?

Min: in the limit that debt/GDP is infinity, rates have to be zero for debt to be serviceable. So then you will have to use some other method than rates to stabilize inflation. Unless you believe in full Ricardian equivalence you should be fine. (Are the Chartalists right…or am I missing something obvious?)

That 90% debt to GDP ratio was followed by an unprecedented and unfollowed period of GDP growth. Maybe we need to up our debt into that region for a year or two, then sit back and let the economy roar for the next twenty years or so.

K: “in the limit that debt/GDP is infinity”

Well, let’s see, if GDP -> 0 while debt does not, debt/GDP -> infinity. OK, but that is true for X/GDP, so debt does not matter. The problem is with GDP.

OTOH, if debt -> infinity while GDP does not, then the problem is debt, right?

Unless there is some reason to believe that debt inhibits GDP in a way that is not reflected in interest/GDP or deficit/GDP, what is the point of the debt/GDP ratio? There is a temporal mismatch between the two variables.

Oops!

I said, “while GDP is a measure of growth.” There is my confusion. It is delta(GDP) that is a measure of growth, right?

However, my question remains, why do people think that debt/GDP is significant to start with?

Thanks. 🙂

Simon, in the post you say “Krugman doesn’t dispute the data; he disputes Rogoff’s use of it to urge for fiscal restraint. I’m trying to understand their conflicting points of view, but here’s my take on it so far. ” You then proceed to list 2 bullet points with points Krugman has made.

The very next paragraph begins “One feature of the Reinhart-Rogoff paper that strikes me is that they only seriously consider the possibility that debts cause low growth.” Now, since the point about low growth being the causal factor in high debt/GDP has not yet been made it appears that this point is the important part of the sentence. That is, it appears you are presenting the point as one that Krugman missed. Yet Krugman had made this point repeatedly, it featured prominently in everything he has written about this paper by R&R.

In the comments you claim that the point you were making was about R&R only stressing the one direction of causality, that you were just critiquing R&R and not making a point Krugman missed. If that was the case why not list the point as number 3 of Krugman’s arguments and then proceed to critique R&R for missing it? It then would have been quite clear that you were not presenting the point as new. Instead, since the point about low growth being the causal factor has not yet appeared in context, your sentence appears to be making that point and not simply criticizing R&R for missing it.

As for the tone of my comment it was I rude I agree, with hindsight I should have made the point more gently. However, the reason for my tone was that it was carried over from the last post you made and I had commented on where you were quite rude and condescending so I felt I was responding in kind. What was annoying was that you had been condescending in a response that was quite idiotic and completely irrelevant to what I’d said, all you did was show yourself to not understand some pretty basic economic theory.

So, while yes I could have ignored it, and probably will ignore you in the future, the rude tone began with you. And, while I can certainly see why your so intellectually insecure I’d suggest that if you really are so sensitive then blogging isn’t for you.

Simon@07:31AM:”I did not know that I was repeating Krugman’s arguments.”

And maybe Krugman did not know that he was repeating Neo-chartalist’s argument here.

Min: I was agreeing with you. I was trying to explore the conditions for high debt/GDP to be stable. But I obviously didn’t make my point very clearly…

If deficits cause debt to grow very big, i.e. debt>>GDP, then rates must go to zero. Otherwise debt becomes unserviceable. At this point it is necessary to have deflation in order to have a stable growing economy, since roughly r = growth+inflation. In order to control deflation at the level of expected growth, one would have to use fiscal policy since the short rate (and the whole curve) is stuck at zero.

Min:

I think that many who look at Debt/GDP ratios are using this as a rough-and-ready way to normalize debt and get a handle on the ability to service the debt. Note that in the financial industry, loan officers and auditors frequently look at debt/income ratios (among other things), so analogs appear to have been useful.

That said, it is clearly a measure that suggests may improvements. You’ve suggested interest/GDP, foreign debt service/GDP, which are also used and offer some advantages. I don’t have a good reason why these are not more widely used. Perhaps because they are subject to much more rapid changes as interest rates and exchange rate vary? Anyone have a better idea?

westslope Not to my knowledge. Want to give it a try? If I were a betting man, I’d worry that confidence has much more short-term variation while Debt/GDP evolves much more slowly, but checking it out beats armchair speculation any day of the week.

Or, to put it in your terms:

To fix the “temporal mismatch” it makes sense to compare growth to debt*r. If debt->infinity r must go to zero.

himaginary: Nice link. I’m sure there’s more that discuss the ambiguity of causality in this case.

Adam P.: Let’s rewind the tape. The first thing I say after discussing Krugman is “One feature of the Reinhart-Rogoff paper that strikes me is that they only seriously consider the possiblity that debts cause low growth.” That’s also what I meant. Read their paper. They discuss reasons why high debt may cause low growth. They do not do the reverse. Others (the Krugman posts that you quote, the Neo-Chartalist post above among them) say the causality could go from growth to debt. The (much earlier) prominent paper that I cited provides more evidence on the historical role of such growth in the US case. If others stated that the original R&R paper presented only one side of the case, then I missed it and, sad to say, I’m still missing it.

“What bothers me here is that Ken is using the authority of a fine, careful empirical study to support policy recommendations that aren’t actually grounded in that study, and also happen to be at odds with his own economic models.”

That’s how Krugman concludes the comment that I linked in the first sentence of my post. My simple point in the paragraph to which Adam P. objects was just that this fine, careful empirical study is already skewed.

Why should a government be in perpetual debt? I don’t quite understand that. Do you mind providing a pointer?

I guess I have in mind that governments go on forever (which seems weaker than assuming (as is done routinely in finance circles) that the US government will always honour its T-bills). Why should there always be a debt to pay off?

Stephan

Simon,

If you read Paul Krugman’s piece closely, I think you’re mistaken about which study he is calling “fine” and “careful” (although he does leave it ambiguous). There is a book, which he praises effusively, and then there is a paper, which he describes as being “not up to the standard” of the book. My understanding of the statement you quote a few comments above this is that Rogoff is using the authority of the book (not directly, of course, but by implication, because it’s a study of the same subject by the same authors) to support the conclusions of the paper.

K: “I was trying to explore the conditions for high debt/GDP to be stable. But I obviously didn’t make my point very clearly…”

Thanks, you were clear enough. I was just trying to disentangle the import of the ratio. 🙂

Simon van Norden: “I think that many who look at Debt/GDP ratios are using this as a rough-and-ready way to normalize debt and get a handle on the ability to service the debt. Note that in the financial industry, loan officers and auditors frequently look at debt/income ratios (among other things), so analogs appear to have been useful.”

Thanks, that’s helpful. 🙂

Simon: “That said, it is clearly a measure that suggests may improvements. You’ve suggested interest/GDP, foreign debt service/GDP, which are also used and offer some advantages. I don’t have a good reason why these are not more widely used. Perhaps because they are subject to much more rapid changes as interest rates and exchange rate vary? Anyone have a better idea?”

To be somewhat cynical, if you look at interest/GDP for the U. S. today, it is not at all scary. 😉 You can scare people with debt/GDP, though.

I thought Krugman’s forte was international trade. Though I guess there was a path-dependent growth angle aspect to it as well, I thought he was a proud microeconomist (considering the reputation macros have these days, not such a bad thing to be).

My impression is that Krugman made his reputation mostly with major contributions to the study of international financial crises (with his speculative attack models), the study of international trade (with his monopolistic competition models) and the study of growth (with stuff on economic geography that I know much less about.) I was thinking that the first and the last of these mattered most for this debate. The second one was probably why some would peg him as a “proud microeconomist.”