The Department of Finance publishes monthly numbers for how much money it has taken in, and how much it has spent. It chooses to run these numbers on the afternoon of the last Friday of the month these days. I'm pretty sure that when the feds were running surpluses, these numbers were released first thing on Monday mornings.

Anyway, the numbers for February were released last Friday. And there were some encouraging signs in there.

The monthly numbers have a significant seasonal component. For example, there's a whole whack of spending in March as managers push through last-minute items: they know very well that the reward for not spending all the money allocated to them is a budget cut. So the numbers below are for 12-month moving sums. These do not necessarily correspond to the numbers for the fiscal year, but they give us a pretty good idea of where we are.

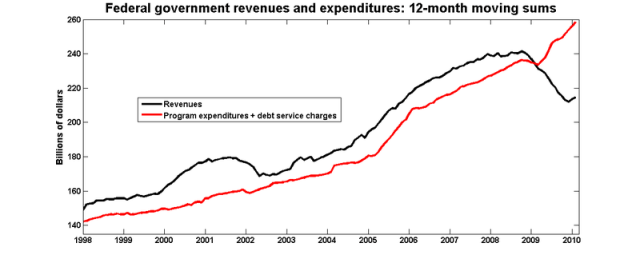

Here is a graph of federal spending and revenues

Here's a thing to remember: the increase in federal spending didn't start until April 2009. During the worst of the recession, spending was actually falling.

The sharp increase in spending associated with the stimulus package is evident from that graph, as is the drop in revenues as economic activity slowed. But the 12-month moving sum of revenues bottomed in December, which surprises me somewhat. How and why did that happen?

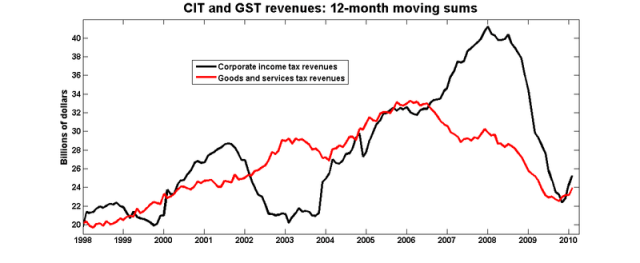

The answer is not in personal income tax revenues. As ever, employment growth is a lagging indicator in this recession, and PIT revenues haven't yet begun to recover. What has come back are revenues from the GST and corporate taxes:

The GST numbers are consistent with the standard narrative of how the business cycle played out, bottoming out last October.

But the CIT numbers seem almost too good to be true. I was expecting them to fall well below the levels of 2002-03, since the 2008-09 slowdown was much, much more severe. And I was also expecting them to stay low for at least a year or two as in 2002-03: since past losses can be written off, it should have taken a couple of years of profitability before CIT revenues started bouncing back.

These trends are only four months old, but it would be very good news indeed if they held up. If growth in consumer spending and profits continues, then the outlook for employment is very encouraging.

I was surprised to see just how volatile CIT revenues are, though I expect I shouldn’t be. Yep. That’s gotta be the main story.

Eyeballing your top chart, it looks like the deficit peaked at around $42 billion, which is a good $10 billion better than we expected. I wonder whether the loans to the automakers and others are included there?

Pleasantly surprised? I know I am.

It is curious that in the background stock markets and commodity markets have corrected sharply in the last couple of days. Ostensively on fears of Greek fiscal contagion. The fear seems overblown to me. I see a constant trickle of positive news out there and what appear to be various forecasts revised upwards.

Maybe these markets just needed a pretext to calm down?

It seems to me that CIT revenues have emulated our TSX with at least a 6 months lag. The drop in revenues has been around 45% and for the index it has been around 50%. Now, the rally from the lows is in the range of 55-60% and that probably means an increase for CIT revenues of the same magnitude. That is, roughly, an additionnal 10 billions $ at least for the government.

Maybe the market is wrong…who knows!